What a new Mister opening does to the wash next door

Mister Car Wash opened 42 new sites in the U.S. between January 2024 and April 2026. This post measures what happened to nearby incumbent car washes after each of those openings.

The headline number

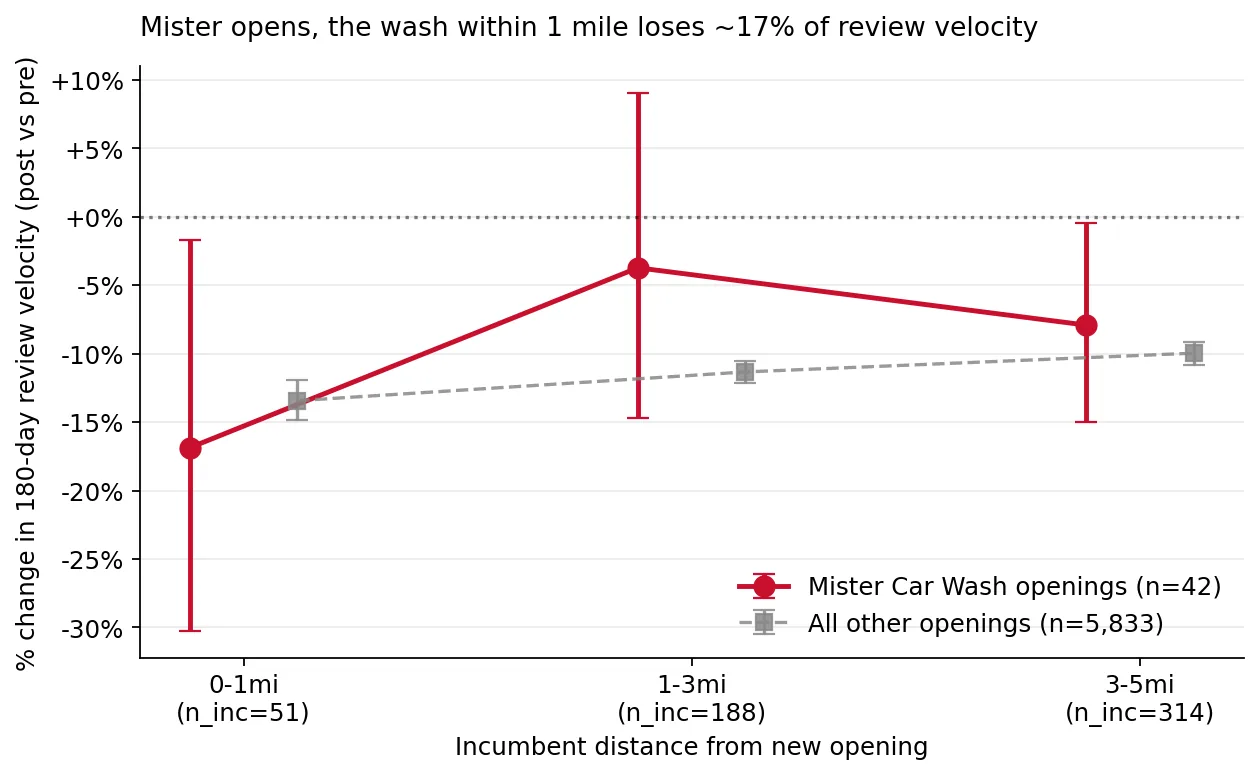

For each of the 42 openings, we compared Google review velocity at every existing car wash within 5 miles, in the 180 days before vs. the 180 days after the opening date.

At incumbents within 1 mile of a new Mister, review velocity drops about 17% on average. 95% CI [-30%, -2%], n=51 incumbents across 31 openings with a 1-mile neighbor.

For comparison, the dataset-wide average for new express openings is roughly a 14% drop at 1 mile (see our broader car wash cannibalization study for the full curves and methodology). Mister’s shadow is a touch heavier than the typical new tunnel, but not dramatically so — Club Car Wash, for example, is closer to -27% in the same 1-mile band. Quick Quack is around -10%. Mister sits in the middle of the express pack.

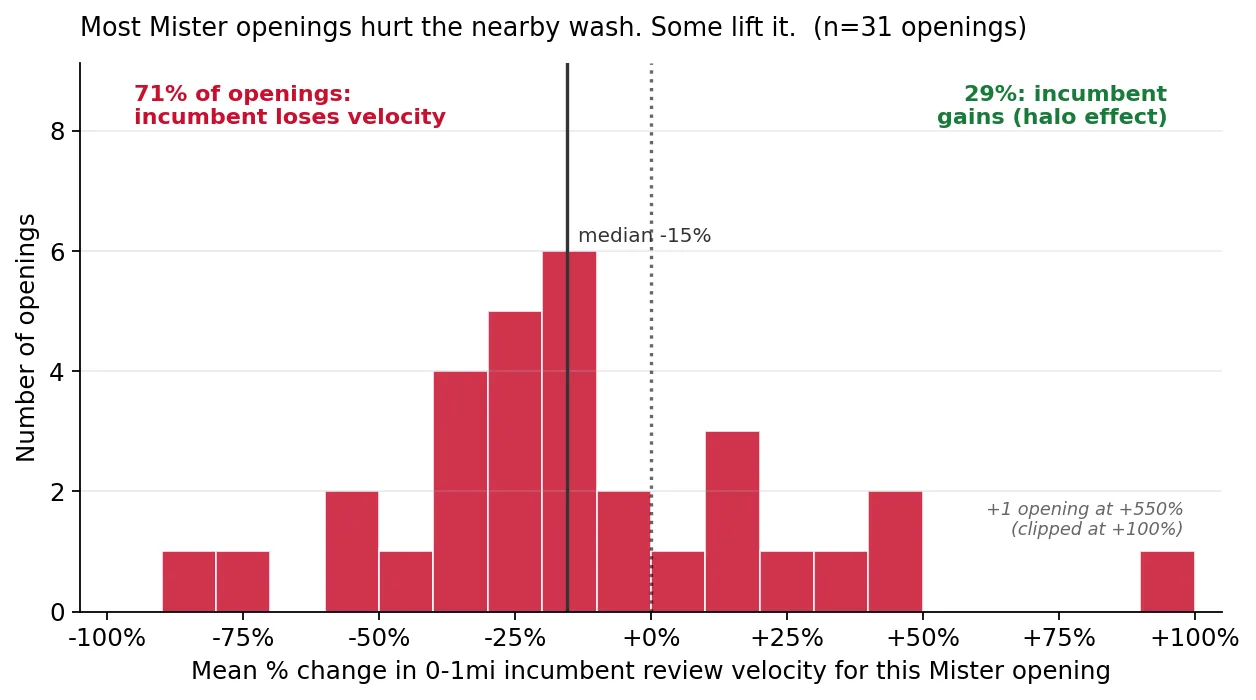

Most incumbents get hit. A few get a lift.

The median 1-mile incumbent loses 13% of its review velocity. 41% of incumbents lose more than 20%. 28% lose more than 40%.

But not everyone loses. About 30% of Mister openings actually coincide with a gain in review velocity at their nearest neighbor. Two MN openings, two TX, and one FL all show a meaningful lift. Best guess on mechanism: a new Mister pulls a wave of “first-time-trying-the-express-thing” customers into a corridor, and the small operators next door catch some of the spillover. The shadow has an edge of halo.

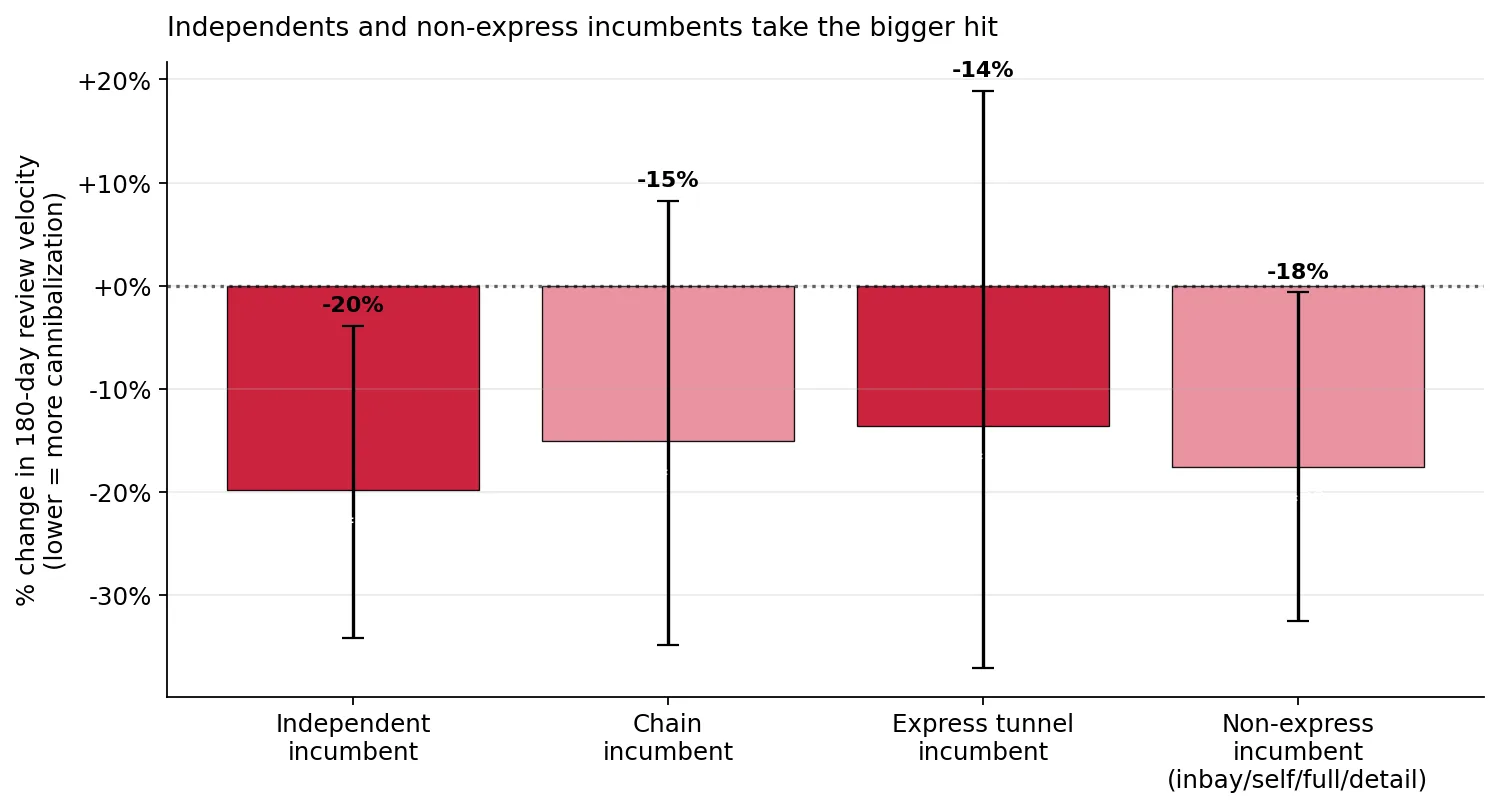

Who actually loses

This is the more useful slice:

| Incumbent type | 1-mi velocity change | n |

|---|---|---|

| Independents | -20% | 19 |

| Other chains | -15% | 32 |

| Express tunnels | -14% | 22 |

| Non-express formats (inbay, self-serve, detail, full-service) | -19% | 29 |

Two patterns worth sitting with:

-

Independents get hit harder than chains (-20% vs -15%). Chain incumbents have membership programs that lock customers in for a billing cycle; independents are mostly pay-per-wash, and the customer can defect to the new Mister with zero switching cost.

-

Non-express formats get hit harder than other express tunnels. This is counterintuitive — you’d think the closest substitute (another express) would bleed the most. It doesn’t, because express-to-express customers have monthly memberships. The wash that really suffers is the inbay-automatic at the gas station, the self-serve bay, the full-service operator. Customers were using them as the convenient option. Mister is now the convenient option AND the better wash.

The worst single-format hit in our Mister-incumbent sample is detail shops at -55%, but n=2 so don’t quote that without flagging the sample size.

The error bars on these subgroups overlap — the differences are directional rather than statistically separable on a sample this small. But the ordering (independents > chains, non-express > express) matches the same membership-stickiness story that shows up in the headline cannibalization data on the full opening sample.

Stars don’t move

This is the same finding as the headline cannibalization study, and it shows up cleanly here: average star rating at 1-mile incumbents barely changes (-0.009 stars). Customers aren’t getting angrier at the old wash. They’re just going less often. Cannibalization shows up in quantity, not quality — which is exactly why operators who only watch their Yelp/Google rating miss it until membership cancellations start coming in.

Mister opens into markets that are already crowded

Median Mister opening has 4 other express tunnels within 5 miles. Only 2 of 42 had zero express competition in that radius. 60% had 3 or more.

Translation: this is not a brand picking off greenfield. It’s a brand entering markets where express tunnels have already proved out, and taking share from the existing operators. Combined with our saturation-curve finding (the 3rd express tunnel into a market causes about double the per-incumbent damage of the 1st), this means a Mister opening into an already-3-tunnel market is one of the harder events an independent operator can absorb.

Geographically, the 42 openings cluster in TX (7), FL (6), MN (6), CA (5), and AZ (3). Sun Belt suburbs plus the Twin Cities corridor.

The shadow is contained to one mile

At 1-3 miles, the velocity drop falls to -4% (not statistically distinguishable from zero). At 3-5 miles, -8% — slightly negative but in the noise range you’d expect from secular trends, not from the Mister event itself.

In other words: if you operate a wash and the new Mister is going up across town, the data says you’ll probably be fine. If it’s going up across the street, the median outcome is a real and persistent decline in throughput.

What to do with this if you’re an operator

- The “what’s my exposure” question reduces to a one-mile question. Don’t fret about Misters opening 4 miles away. Worry about the one going up next to you.

- Membership is the moat. The express incumbents in our sample lose less than the inbay/self-serve operators, and chain incumbents lose less than independents — both gaps point at the same thing. If you’re an independent with no membership program and a Mister is breaking ground at the next intersection, your retention strategy needs to be in place before the soft open, not after.

- Review velocity is what an outside analyst uses because it’s the only signal that’s public. If you’re the operator, your POS, wash-count, and membership-churn data will move first and tell you the real number. Review velocity is useful for benchmarking against peers you don’t have books on — not for managing your own site.

Caveats, in plain English

- n=42 openings, n=51 incumbents in the 1-mile ring. The point estimate is robust enough to publish but the confidence interval is wide — true effect could plausibly be anywhere from -35% to -2%.

- Review velocity is not revenue. Express tunnels generate more reviews per customer than self-serve. A 17% drop in reviews probably translates to a smaller drop in dollars, but we don’t have the calibration to say how much smaller.

- The 180-day post-window captures the immediate effect, not the long-term equilibrium. Our dynamic event study (on the full opening sample, not Mister-specific) shows cannibalization peaks at months +2 to +6 and partly recovers by month +12. Mister-specific dynamics are sample-size-limited but appear consistent with that arc.

- Selection. Mister picks specific markets — already-saturated, suburban, decent MHI. The “average” 17% drop is the effect at the kind of incumbent Mister chose to compete with, not a universal Mister coefficient.