When a New Car Wash Opens, How Much Business Does It Actually Steal?

A national, data-driven look at trade-area cannibalization, using 5.9 million Google reviews and every new US car wash that opened in 2024–2025.

- 5.9M Google reviews

- 6,559 new openings (2024–2025)

- 134,000 matched pairs

- 94,000+ analyzed comparisons

- Jan 2024 – Apr 2026

Executive Summary

A national look at trade-area cannibalization, using 5.9 million Google reviews and every new US car wash that opened in 2024–2025. The headline findings in one minute:

- The headline cannibalization effect is the 4-percentage-point gap between washes within 1 mile of a new opening and washes 3–5 miles away. All washes were losing review activity in this period (a national secular trend, not caused by any one competitor) — within-1-mile incumbents lost about 14%, 3–5 mile incumbents lost about 10%. The 4 pp difference is the part attributable to proximity; the rest would have happened anyway. A single new competitor by itself produces almost no measurable damage on top of that secular trend — the visible cannibalization comes from clusters of multiple new openings (see the saturation finding below).

- The damage hits immediately at the opening month and persists for at least a full year afterward. The customer loss is a one-time reshuffle, not a slow squeeze — but the new (lower) traffic level sticks. We see no recovery in the 12 months we tracked; if anything, the gap between affected and unaffected washes widens slightly in the second half of the year.

- The customers don’t go to the wash next door because it’s the same kind of place. They go because they were settling for the wrong kind of place all along. A new full-service wash hurts nearby detail shops worst (down 30%+). A new express tunnel hurts nearby self-serve bays worst (down 27%). Same-format competitors hurt each other least.

- The first new competitor within a mile barely matters. The third is a cliff: existing washes with three or more new competitors within a mile lose around 34% of their reviews — more than double the loss from just one competitor.

- A new car wash opening within the same chain is noticeably less damaging to the existing sister location than a competitor opening — review activity holds up much better. But “less damaging” isn’t “free”: review volume is a proxy for traffic, not for sales per location. Members who split their visits and walk-ins who redistribute between sister sites can quietly erode per-location revenue even when review counts look stable. The right framing is customer transfer, not customer loss — better than competitor entry, but not zero impact at the unit level.

- Customer satisfaction is not a moat. The highest-rated existing washes (4.8+ stars on Google) lose about 31% of their customers when a new competitor opens — the worst outcome of any rating band. The most resilient washes are middle-rated (4.0–4.2 stars).

- Cannibalization is 2 to 3 times steeper in the Northeast and West than in the Midwest and South. A new competitor in New Jersey is roughly twice as damaging to an incumbent as the same competitor would be in Wisconsin.

How much business does an existing wash actually lose?

We looked at every new car wash that opened in the United States between mid-2024 and late 2025 — 6,559 sites in total. For each one, we found every existing car wash within 5 miles (about 134,000 matched pairs in all) and measured how much customer activity the existing wash had in the 6 months before the new wash opened versus the 6 months after.

Customer activity is measured here through Google reviews. We’re not measuring revenue — Google reviewers are a subset of customers — but the same proportion of customers leave reviews at every wash, so changes in review counts reliably track changes in customer traffic.

The headline finding — and the right way to read it:

Every wash in this dataset was losing review activity over 2024–2025, regardless of competition. It is a national trend, not anything specific to any one wash or any one new opening. Across the whole sample:

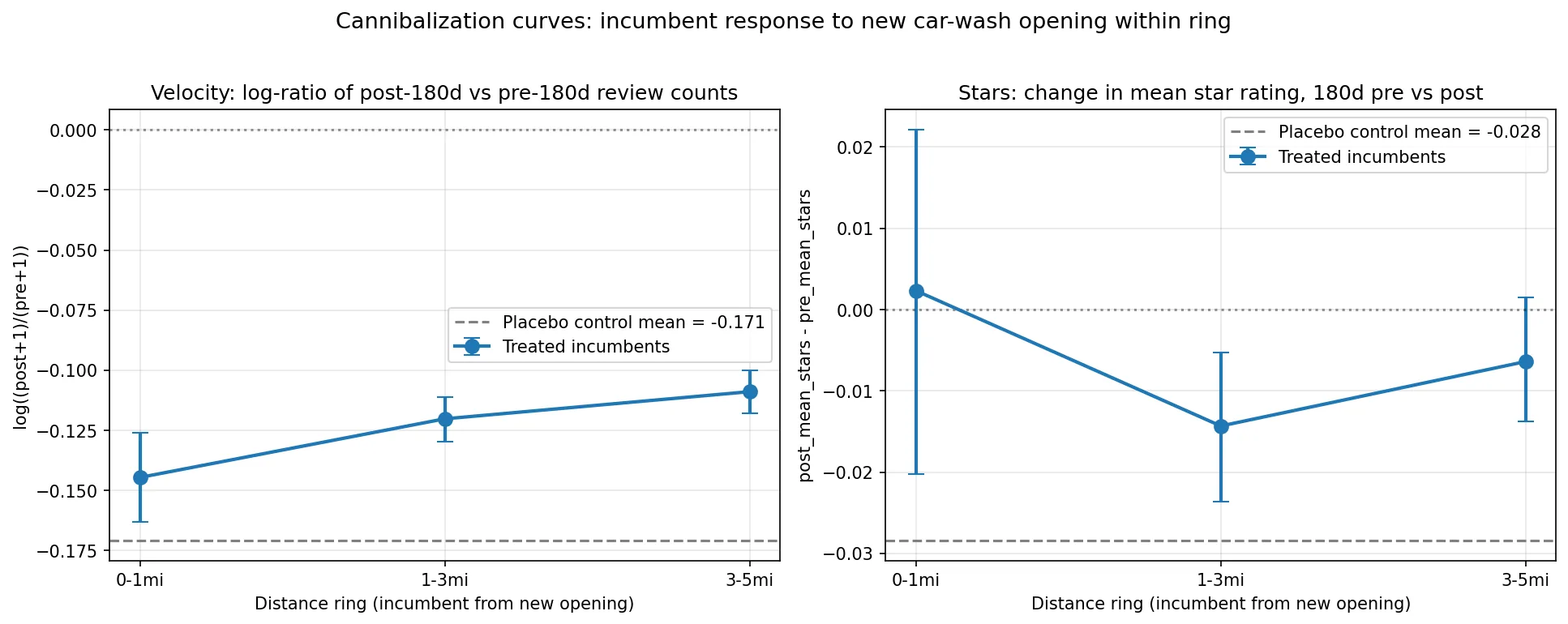

- Existing washes within 1 mile of a new opening: lost about 14% of their review activity over 6 months.

- Existing washes 1 to 3 miles away: about −12%.

- Existing washes 3 to 5 miles away: about −10%.

- Existing washes with NO new opening anywhere within 5 miles: dropped roughly −17% over a comparable window.

That last number is the most important one for reading the others. A wash with no nearby competitor entry was still losing about 17% of its review activity during this period. So the 14% drop at the within-1-mile washes isn’t “caused by the new competitor” — most of that 14% would have happened anyway.

What IS caused by the new competitor is the 4 percentage point gap between the within-1-mile group and the 3–5 mile group. Both groups operate in the same kind of market with the same secular pressures; the only systematic difference is proximity to a new opening. That 4 pp gap is the cannibalization effect.

Star ratings barely move at any distance. Customers aren’t getting worse service — there are just fewer of them.

This is real but moderate. It is not a “the new wash will kill the old wash” story. It is a “the new wash takes a few-percentage-point bite, and the old wash keeps operating” story.

One important nuance, picked up in more detail below: that 4 pp average is heavily influenced by washes that had multiple new openings nearby. A single new wash on its own produces almost no measurable damage. The real cannibalization shows up when 2, 3, or more new washes open in the same trade area inside 18 months — see the cliff finding further down.

When does the damage actually happen?

A common expectation is that customer loss from a new competitor is gradual — customers slowly drift away over a year. The data says otherwise.

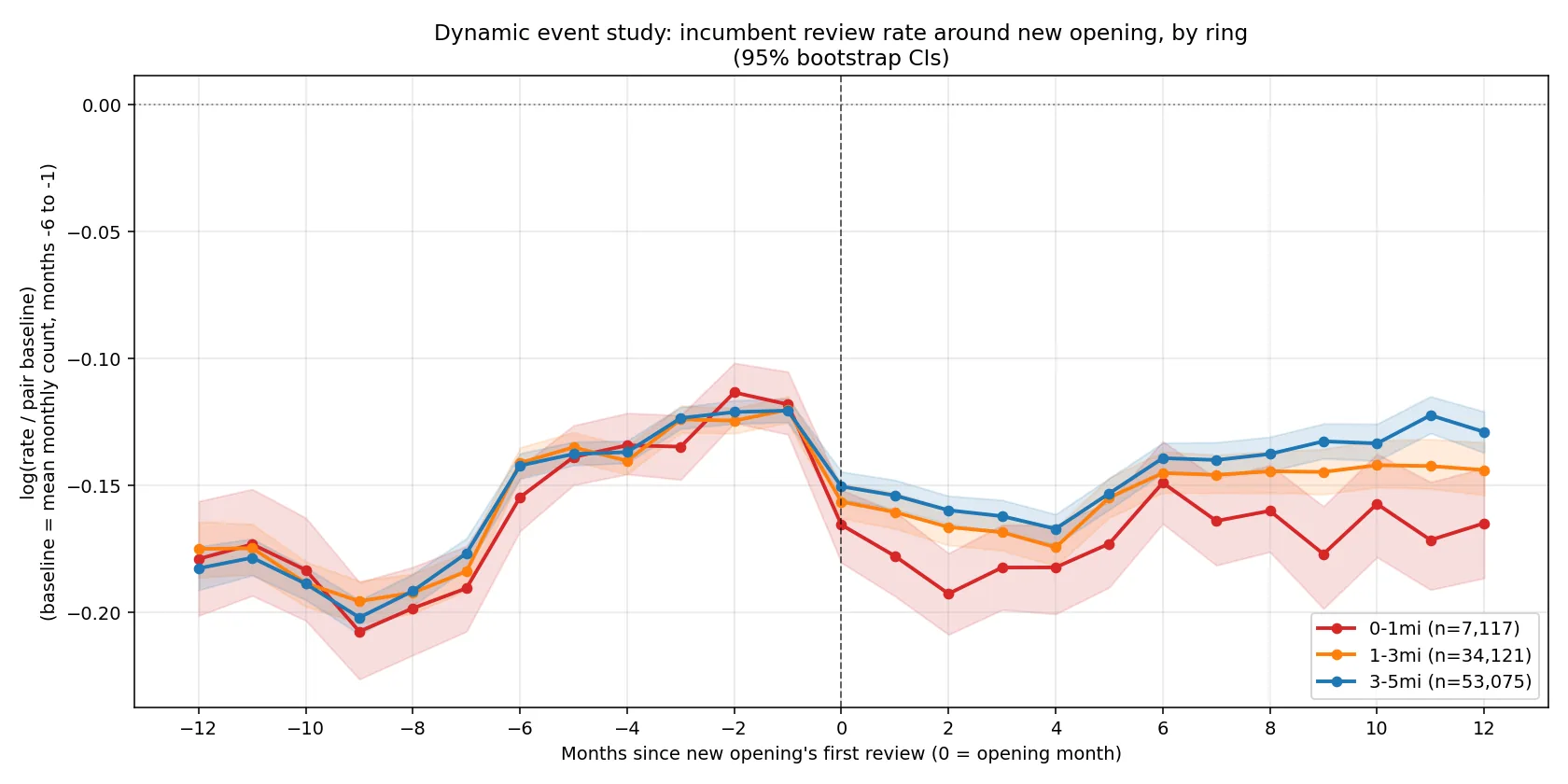

Looking at month-by-month review activity at existing washes, from a year before the new opening to a year after:

- Before the opening: all groups (washes within 1 mile, 1–3 miles, 3–5 miles) track each other almost perfectly. This is the most rigorous test of the analysis — washes at different distances would have evolved similarly if the new opening hadn’t happened.

- At the opening month: the 1-mile group dips below the others. The gap is small at first.

- Months 2 through 6: the gap is widest. Within-1-mile washes are running roughly 5% below the 3–5 mile group on a monthly basis.

- Months 7 through 12: the gap persists. There is no recovery in the year following the opening. If anything, the spread between within-1-mile washes and washes 3–5 miles away is slightly wider in months 7–12 than in months 1–6.

The mechanism appears to be a one-shot reshuffling of customers, not an ongoing erosion. Customers try the new place, some of them stick with it, and the existing wash settles at a new, lower traffic level — and stays there. We see no evidence of the lost customers coming back inside 12 months.

Who actually competes with whom?

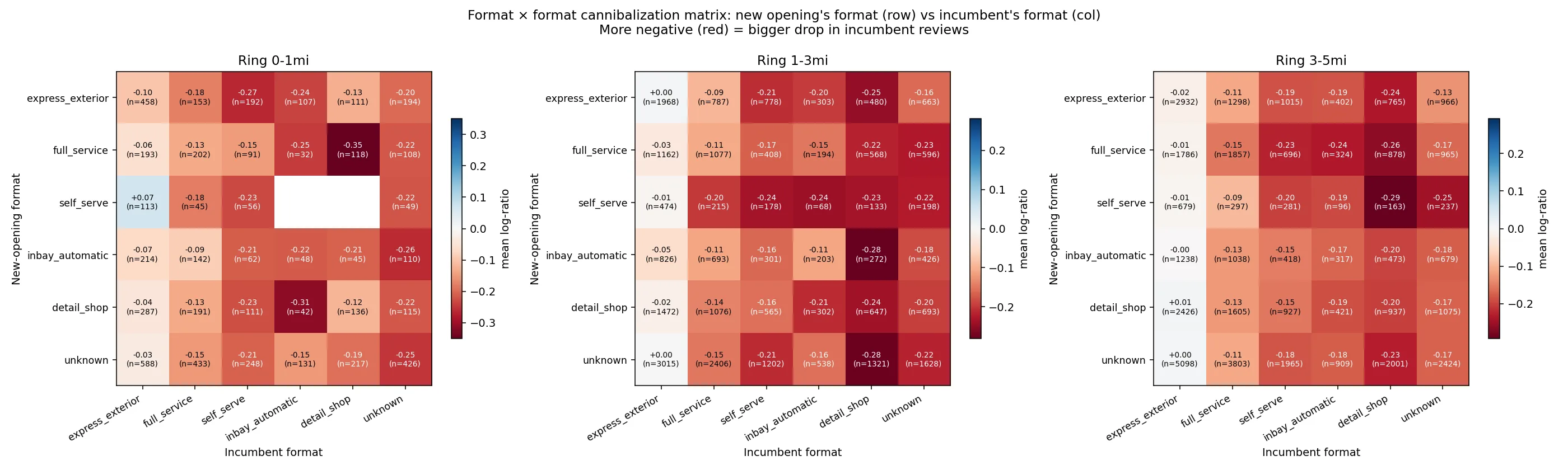

The intuitive answer is “competitors of the same type compete most fiercely with each other.” Two express tunnels next to each other should hurt each other more than an express tunnel and a self-serve bay.

The data says the intuition is wrong.

The most-damaged existing washes are the ones whose customers were settling for the wrong kind of wash all along — and finally have a better option open nearby:

- A new full-service wash opens within 1 mile of a detail shop. The detail shop loses about 35% of its review volume — the single worst combination in the data. Detail shops and full-service washes both target the “I want my car cleaned thoroughly” customer; when a full-service wash shows up, the detail shop loses much of that pool.

- A new express tunnel opens within 1 mile of a self-serve bay. The self-serve bay loses about 27%. Self-serve customers are price-and-convenience driven; an express tunnel offers a much faster, easier experience for similar money.

- A new express tunnel opens within 1 mile of another express tunnel. The damage is much milder — about 15%. Same-format markets tend to settle into stable equilibrium pricing and membership programs; a marginal new entrant expands capacity rather than displacing customers.

The general pattern: new entrants pick off the customers who weren’t a great fit for what they were using. Direct same-format competitors don’t take much from each other once a market has settled.

How bad is it when two new competitors open near you?

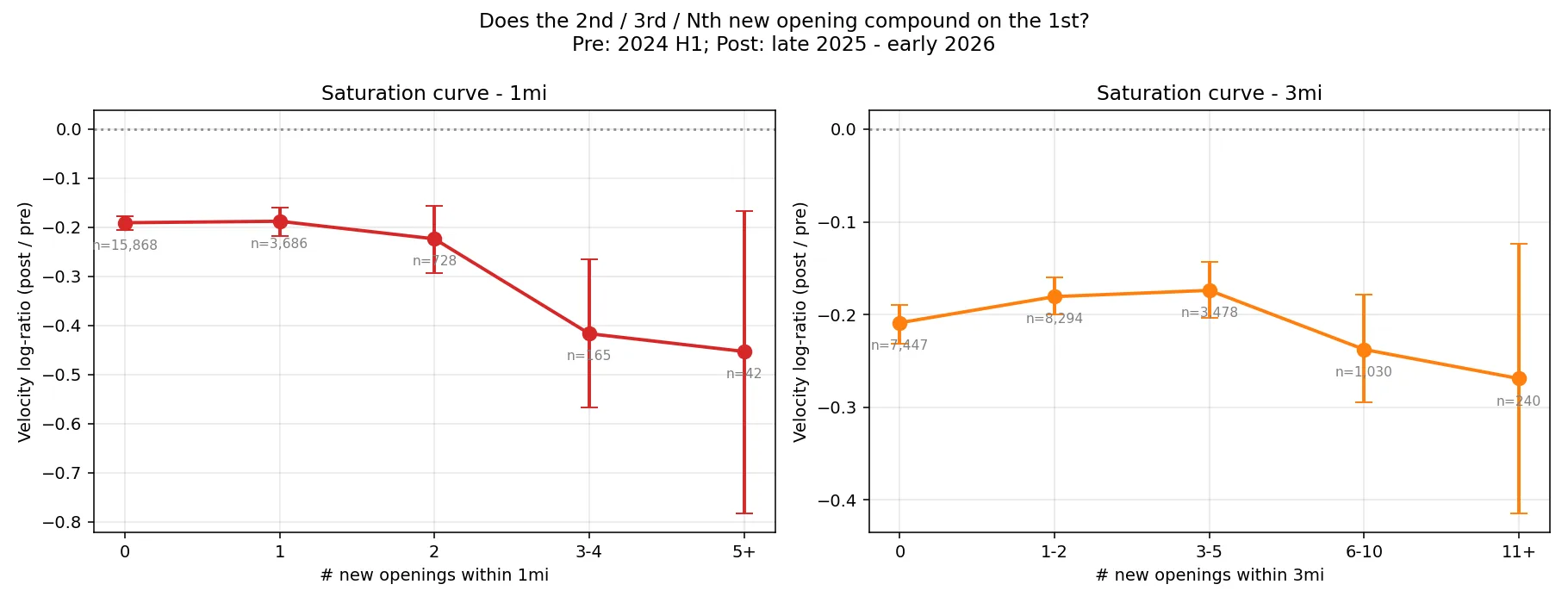

The simplest assumption is that two competitors are twice as damaging as one. The data shows the relationship is much more abrupt than that.

Looking at existing washes by how many new washes opened within 1 mile of them in the same 18-month period:

| Number of new washes within 1 mile | Approximate loss in customer activity |

|---|---|

| 0 (the secular baseline — everyone is dropping a bit) | ~17% |

| 1 | ~17% (no extra damage) |

| 2 | ~20% (small extra damage) |

| 3 or 4 | ~34% (more than double the baseline) |

| 5+ | ~36% |

The key pattern: the first new competitor is essentially free. An existing wash with one new competitor within a mile is statistically indistinguishable from an existing wash with zero new competitors. The second adds a small bit of damage. The third hits like a cliff — the loss roughly doubles.

This shifts how to think about competitive pressure. A new wash opening across the street is not, by itself, a strategic emergency. But if a second and third one show up in the same trade area inside 18 months, the existing wash is in real trouble — fast.

Same chain opening nearby? Less damage — but not zero.

A specific case worth highlighting: what happens when the new wash is a different location of the same chain as the existing one?

The data shows review volume at the existing same-chain location holds up much better than when a competitor brand opens. At 1–3 miles, where our sample is large enough to be confident (about 500 same-chain pairings), customer review activity at the sister location is essentially unchanged. At 3–5 miles, the same.

At 0–1 mile, however, the picture is less clear. We have only 83 same-chain pairings that close — not many — and the data is consistent with anywhere from “no effect” to “as bad as a cross-chain competitor opening.” We just can’t tell from review volume alone at that proximity.

Important caveat: review volume is a proxy for customer traffic, not for sales per location. Even if the same number of customers continue to leave reviews at the original site, a few things can quietly erode that site’s economics when a sister location opens nearby:

- Members splitting their visits between the two locations. A monthly-pass holder pays the same regardless, but if they used to do five washes a month at site A and now do three at A and two at B, site A has lost 40% of its per-visit revenue opportunities (upsells, premium-tier washes, vacuum-bay traffic).

- Walk-in (non-member) customers splitting between locations. Walk-ins are typically the highest-margin customers; if they redistribute across two sister sites, both sites’ walk-in revenue drops even if total chain revenue is stable.

- Operating costs per customer go up at the original location when its absolute traffic drops, even if the chain’s network is more efficient overall.

So a fair summary: same-chain new builds are noticeably less damaging to a sister location than competitor new builds, on the review-volume measure we can observe. But “less damaging” is not “harmless.” A real-world per-location P&L analysis would almost certainly show some same-chain cannibalization at close distance — we just can’t measure it directly from review data.

For chain operators planning expansion, the right framing is: same-chain infill transfers customers between your sites, where competitor entry loses customers entirely. The transfer is far better economically than the loss — but it isn’t free, and the operator of the existing sister location should expect some real revenue impact at the unit level.

Customer satisfaction does not protect you

A reasonable theory is that the best-run, highest-rated washes should be the most insulated from new competitors. Loyal customers, the thinking goes, stay loyal.

The data says the opposite.

Existing washes sorted by their Google star rating, and how much each tier lost when a new competitor opened within 5 miles:

- Under 3.0 stars (already struggling): about −15% of customers lost

- 3.0 to 3.5 stars: about −7%

- 3.5 to 4.0 stars: about −3%

- 4.0 to 4.2 stars (the safest tier): only about −1% of customers lost

- 4.2 to 4.4 stars: about −2%

- 4.4 to 4.6 stars: about −5%

- 4.6 to 4.8 stars: about −12%

- 4.8+ stars (the highest-rated): about −31%

The pattern is inverted-U. Mid-rated washes — neither great nor bad — fare the best. The very highest-rated washes lose the most.

Why? Two reasons:

- Very high-rated washes are usually small specialty operations (mobile detailers, niche shops) with thin but loyal customer bases. A new competitor in their trade area can take a meaningful share of that small customer pool.

- Mature high-quality markets tend to be multi-loyal markets. Customers who already know the area has good options are willing to try a new good option. Loyalty is to category quality, not to any specific operator.

For an operator: chasing 5-star ratings is not a defensive strategy against competitors. What actually protects existing market share, based on the same data, is: being part of a large chain, being in a higher-income census tract, and being in a higher-density market where there’s enough customer base to absorb a new entrant.

Should you open in a busy market or an empty one?

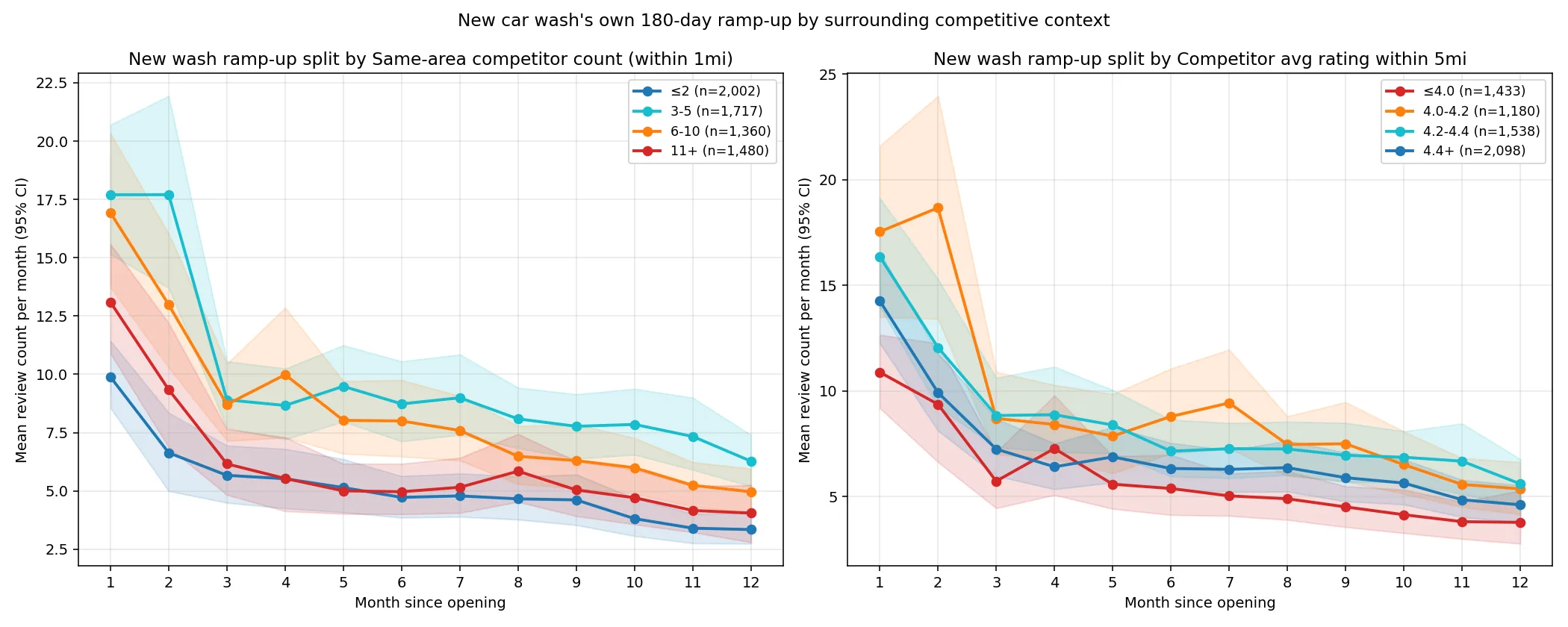

Flipping the analysis around: when a new wash opens, how does the local competitive landscape affect its own customer ramp-up?

The data here also shows an inverted-U — the same pattern as cannibalization severity:

- Markets with 0–2 nearby competitors (empty markets): new washes get only about 10 reviews in their first month, settling around 5 per month after that. The slowest ramp of any bucket. Counterintuitively, “no competition” is the worst place to open — there isn’t enough wash demand in the area to feed a new operator.

- Markets with 3–5 nearby competitors: new washes peak at about 18 reviews in month 1, settling around 9 per month. Joint top performer.

- Markets with 6–10 nearby competitors: about 17 reviews month 1, 9 after. Statistically tied with the 3–5 bucket — also a top performer.

- Markets with 11+ nearby competitors (saturated): about 13 reviews month 1, 5 after. Roughly the same as the sparse end. Too much competition makes it hard to gain a foothold.

For competitor quality (their existing star ratings), the same inverted-U holds:

- Markets with weak existing competitors (under 4.0 stars): new washes ramp the slowest — about 11 reviews in month 1. These are low-demand markets overall.

- Markets with moderately rated competitors (4.0–4.4 stars): new washes ramp the fastest — about 17 reviews in month 1.

- Markets with premium-rated competitors (4.4+ stars): new washes ramp slowly — about 14 reviews in month 1. Customers in high-quality markets are loyal to operators they already use.

The combined siting heuristic: open where there are 3 to 10 same-area competitors with average ratings of 4.0 to 4.4 stars. That’s the data’s sweet spot — enough demand exists (proven by the fact that several competitors can operate at moderate quality), the market isn’t fully saturated, and customers aren’t so loyal to existing operators that a newcomer can’t earn share.

The intuitive picks — either “open in an empty market with no competition” or “open in a premium market” — both produce the slowest ramps in the data. The empty-market case is especially counterintuitive: an “untapped” trade area is usually untapped for a reason (low demand), and the new wash struggles right alongside the absent competition.

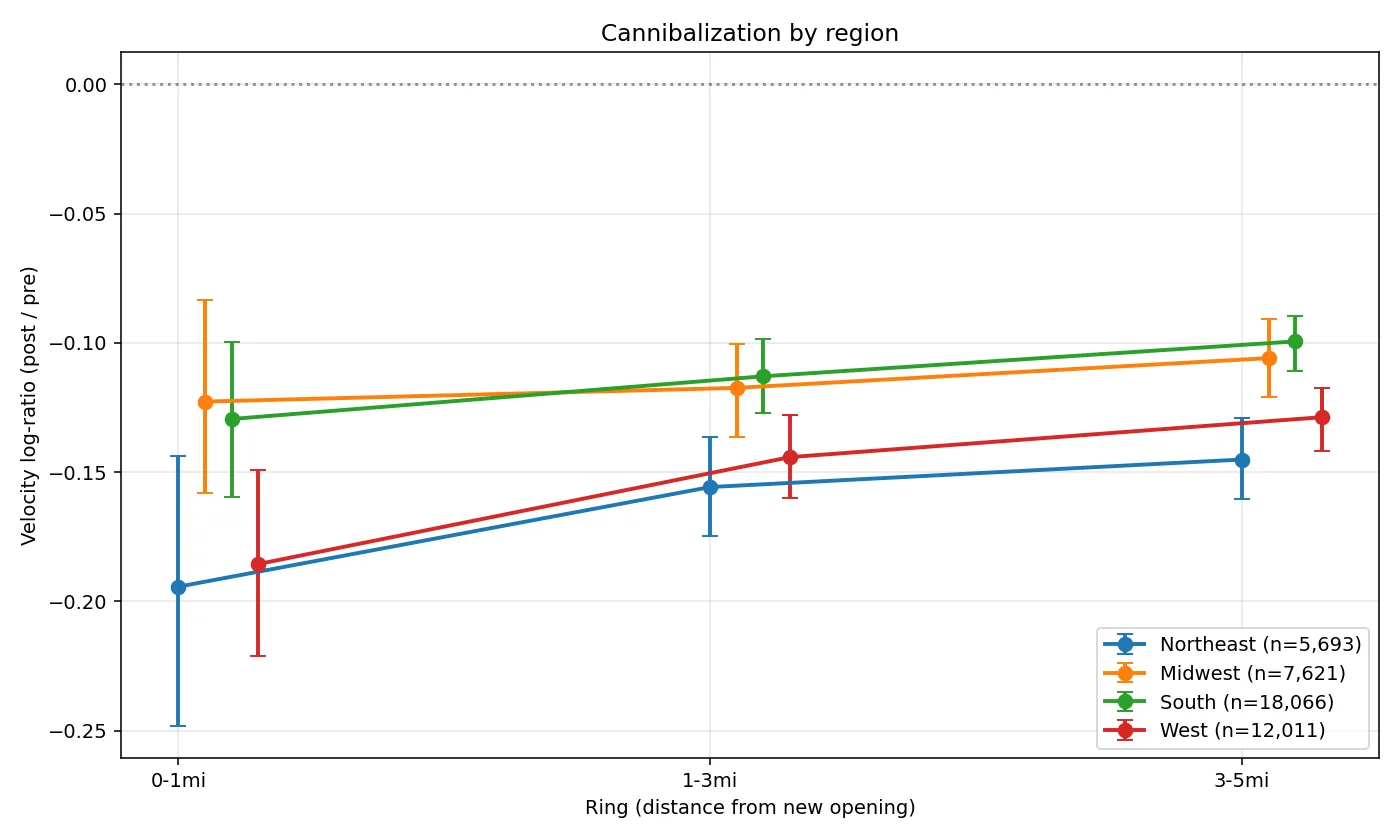

Same effect everywhere? Not quite.

Cannibalization is meaningfully steeper in some parts of the country than others.

By US Census region, the extra customer-activity drop within 1 mile of a new competitor (vs 3–5 miles away):

- Northeast (NY, NJ, PA, MA, etc.): about 5 percentage points of extra cannibalization within 1 mile

- West (CA, OR, WA, AZ, etc.): about 6 percentage points

- South (TX, FL, GA, NC, etc.): about 3 percentage points

- Midwest (OH, MI, IL, IN, WI, etc.): about 2 percentage points — almost flat

In other words, a new wash opening within a mile of an existing wash in the Northeast or West is roughly twice as damaging to that existing wash as the same opening would be in the Midwest. Two possible explanations: Midwestern markets are growing faster (so new builds add to the pie rather than redistributing it), and Midwestern customers may be less inclined to chase the newest option.

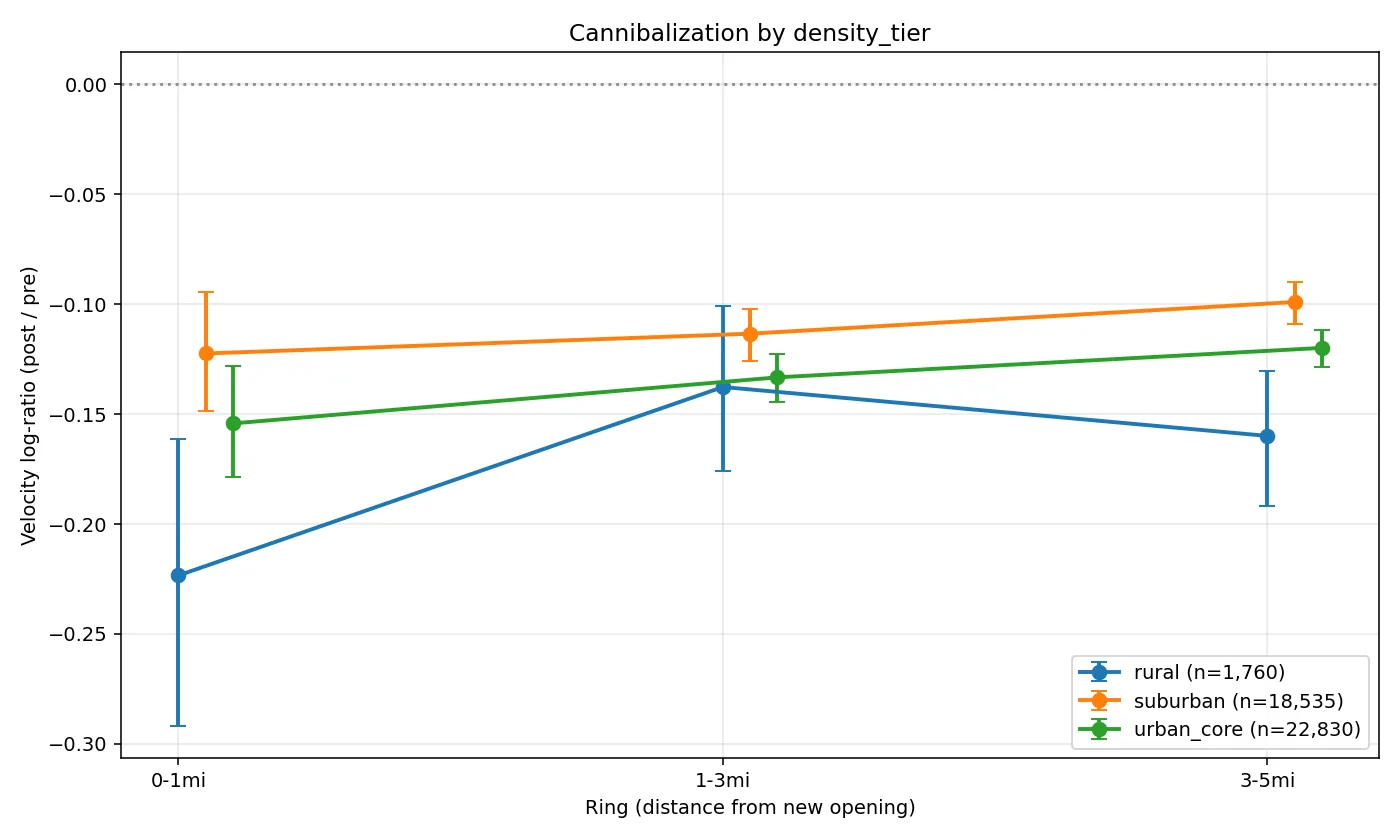

By population density, the rural-vs-suburban breakdown is informative:

- Rural markets are the most fragile at 0–1 mile (−22%) — small customer pools mean a single new competitor takes a disproportionate share.

- Urban core markets sit in the middle (−15%).

- Suburban markets are the most resilient (−12%) — enough customers exist to absorb new entrants without devastating any one operator.

The PE-relevant version of this: the most resilient asset profile is a suburban incumbent in the Midwest. The most fragile is a rural operator in the Northeast or West.

What it all means in practice

For a car wash operator

- A single new competitor opening nearby is a measurable annoyance, not an emergency. Expect a one-time customer drop of around 3–5% above the natural market trend, hitting immediately and persisting at that lower level for at least a year — no recovery in the data so far.

- A second and third new competitor in your trade area within 18 months is the real risk. The damage compounds nonlinearly and a cluster of new entrants can take a third of your business or more.

- The defensive strategy that doesn’t work: chasing a 5-star Google rating. Highest-rated operators are actually the most vulnerable to competition.

- The defensive strategies that do work: scale (being part of a chain), being in a denser/wealthier neighborhood, and operating a format that fits the market (rather than a format your customers are tolerating).

For someone evaluating a wash to acquire

- A 1-mile new-build competitor near the target is real but moderate — about a 3–4% volume hit over 6 months, not a catastrophic blow. Bake it into the model.

- A 3+ new-build cluster within 1 mile in the last 18 months is a much bigger risk — discount aggressively.

- The cannibalization estimate should be regionalized: Northeast and West sites face roughly 2× the cannibalization that Midwest and South sites do. Rural sites are 2× more fragile than suburban ones.

For chain expansion strategy

- Building near your own existing locations is much less damaging than building near a competitor — the customer base rebalances within your network rather than walking out the door entirely. But “less damaging” is not “free”: the sister location should plan for some per-unit revenue impact (split visits, walk-in redistribution), even if review counts look stable.

- Building near a competitor’s existing locations is most attractive when your format displaces theirs — a new express tunnel near a cluster of self-serve bays will displace meaningful customer flow.

- The best new-build site characteristics are: 3–10 same-area competitors of moderate quality (4.0–4.4 stars), in a suburban density tier, in a Midwestern or Southern metro. Sparse markets are surprisingly the worst — no proven local demand.

About this analysis

This study uses 5.9 million Google reviews of US car washes across 174,000+ places, spanning January 2024 through April 2026. New openings were identified as places whose first-ever Google review fell on or after July 2024 (a six-month buffer from the start of the data, to avoid mistaking “first review we have” for “first time the wash opened”). Cannibalization was measured by comparing review counts in the 180 days before and 180 days after each new opening at every existing wash within 5 miles.

The findings reported here come from over 94,000 matched comparison pairs that met the analysis’s quality thresholds. Confidence intervals on the headline numbers are tight; the major patterns are statistically very robust.